The Energy Price Guarantee, announced on 8 September, is expected to add around £100bn to the public sector deficit (and cash shortfall) over the coming year, with a further substantial cost in year 2, according to the Institute for Fiscal Studies. By implication, the OBR’s March forecast of the budget deficit in 2022-23 rises from £99bn to around £150bn, and for 2023-24, from £50bn to about £130bn. Build in a mild recession, and the deficits could easily be £30bn to £50bn higher. Will the Bank of England ride to the defence of the sovereign once more? Or will it stick resolutely to its planned shrinkage of the balance sheet? Gilt investors would like to know.

“But when you give to the needy, do not let your left hand know what your right hand is doing.” In light of last week’s huge fiscal intervention to freeze household energy bills, and soften the burden of business bills, I wonder whether this exhortation (Matthew 6:3) has been taken too literally. The left hand of government has acted again, on a breath-taking scale, comparable to the Covid supports of 2020-21. But the right hand of central banking is intent on reining in its Covid largesse. The Bank of England determined at its 3 August MPC meeting, that “a reduction in the stock of purchased gilts held in the Asset Purchase Facility of around £80bn was likely to be appropriate”.

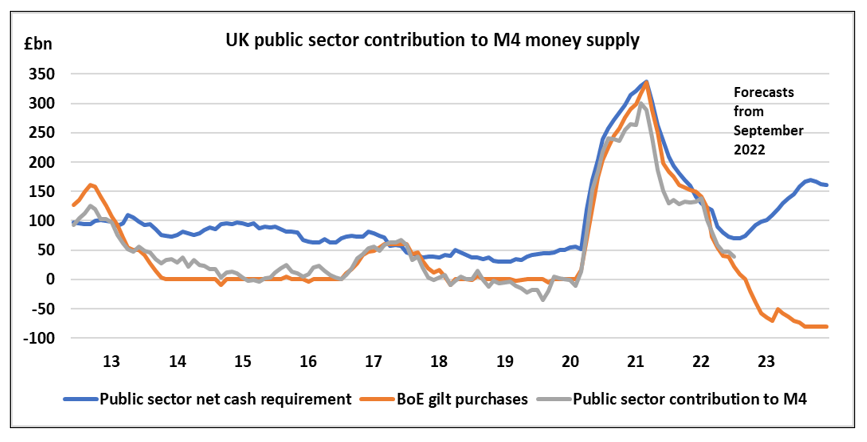

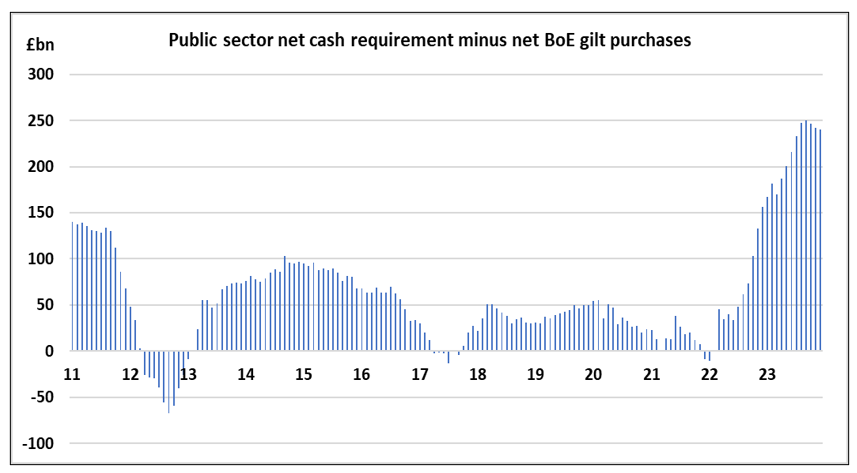

To gauge the magnitude of the chasm between government borrowing and the withdrawal of Bank of England support, please examine figures 1 and 2. The bars in figure 2 show the gap between the public sector net cash requirement and net Bank of England purchases of gilts. Unless the Bank reviews its stance, the annual amount of gilts to be mopped up by the market is set to skyrocket from less than £50bn to possibly £250bn. This, at a time when the UK has the highest G7 inflation rate and when overseas ownership of gilts is tumbling.

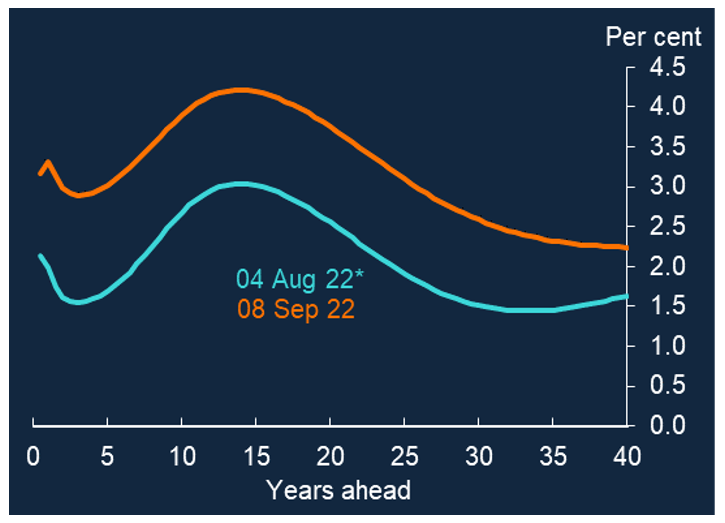

Since the Bank announced its policy on balance sheet shrinkage – all the £20bn of corporate bonds are to be sold off by the end of next year as well as the £80bn reduction in gilt holdings – gilt yields have moved up across the curve (figure 3). We read in a 1 September update that “The Bank will closely monitor the impact of its gilt sales programme on market conditions and reserves the right to amend its schedule (including the gilts to be sold), pricing method or any other aspects of its approach at its sole discretion”.

We stand in eager anticipation of this amendment. Hopefully, the folly of matching the Covid-related budget deficit one-to one with gilt purchases will not be repeated. But without some adjustment of its stance, the Bank will engineer a horrible financial squeeze. Its reputation for monetary competence is hanging by a thread.

Figure 1:

Source: Bank of England and EP forecasts

Figure 2:

Source: Bank of England and EP forecasts

Figure 3: UK gilts: instantaneous nominal forward curve at selected dates

Source: Bank of England