On the M4 definition of the UK money supply, there has been a £125bn contraction (equivalent to 4 per cent) since September 2022. Some of those who sounded the inflationary alarm when annual money growth hit 12 per cent in 2021 are now predicting a collapse into deflation. However, a careful examination of the monetary data suggests that the unwinding of leveraged Liability Driven Investing (LDI) strategies after September 2022 is largely responsible for today’s negative money supply comparisons. M4 holdings of Other Financial Corporations (including LDI vehicles) have fallen by more than 16 per cent since the crisis erupted. While broad money growth, excluding Other Finance Corporations, has slowed to a crawl, this is a natural reaction to a sudden tightening of credit conditions. The ratio of household and non-financial company deposits to nominal GDP remains elevated: the UK retains an inflationary bias in 2024.

By way of background*, LDI products were devised to help a Defined Benefits pension scheme “match” its assets with its liabilities, and to invest in a way that focuses on the scheme’s liabilities, rather than just the scheme’s assets. The closest match for the risks associated with the value of the liabilities is long-term gilts, particularly those linked to inflation. The Pensions Regulator estimated in late 2022 that about 60 per cent of DB schemes have invested in LDI products in one form or another. In the words of a Bank of England briefing to a Treasury Committee, “LDI strategies enable DB pension funds to use leverage (i.e., to borrow) to increase their exposure to long-term gilts, while also holding riskier and higher-yielding assets such as equities in order to boost their returns. The LDI funds maintain a cushion between the value of their assets and liabilities, intended to absorb any losses on the gilts. If losses exceed this cushion, the DB pension fund investor is asked to provide additional funds to increase it, a process known as rebalancing”.

During the September 2022 crisis, many pension schemes did not have sufficient liquid assets to meet their provider’s (very urgent) collateral calls to increase the “cushion” referred to in the Bank of England letter. Many pension schemes struggled to find the required cash in such a short timescale (even highly liquid assets such as equities can take several days to sell) and this also meant that many had to sell gilts, thereby reducing their value further. As gilts prices fell, there was a risk of the entire cushion being eroded, leaving the LDI fund with zero net asset value and leading to a default on the borrowing, meaning the bank counterparty would take ownership of the gilts. The mini-budget of 23 September emitted a shock larger than the Regulator had envisaged and evidently greater than the size of shock the LDI market could withstand. It set in motion an aggressive de-leveraging that has infected a wider range of counterparties in the OFC sector.

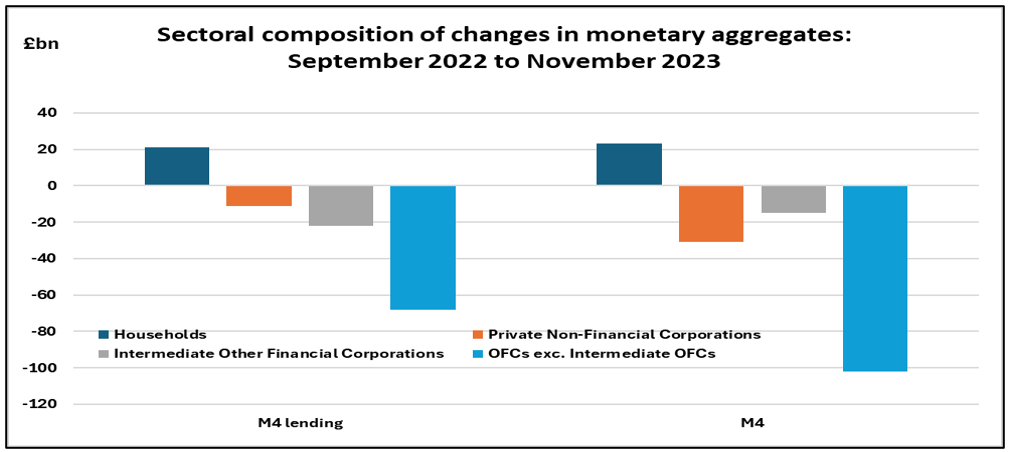

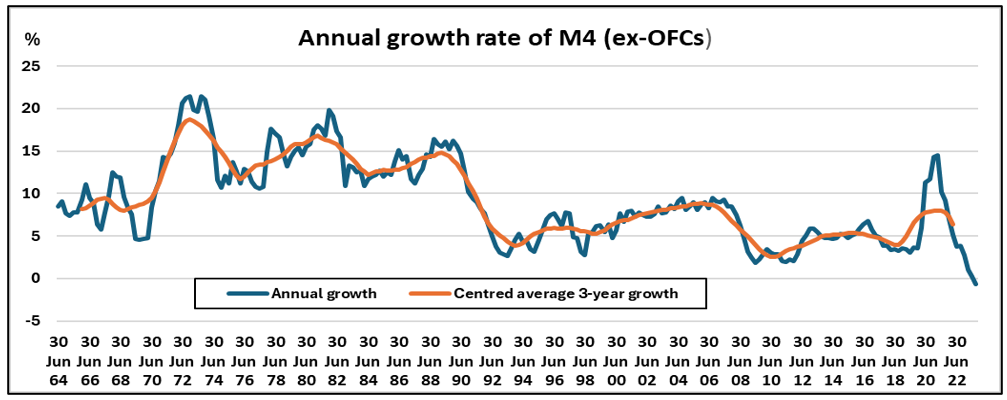

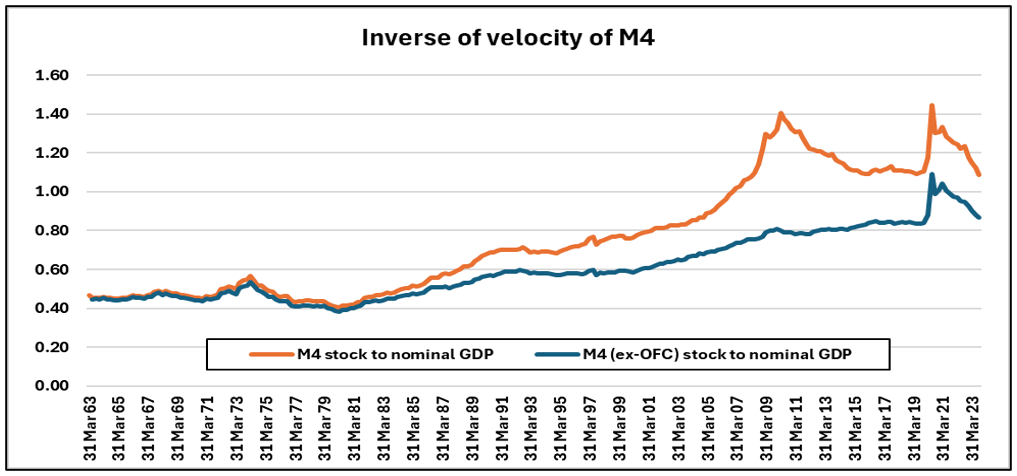

The composition of the shrinkage in M4 since September 2022 is shown in figure 1. The annual growth rate of the combined household and PNFC M4 stock is given in figure 2, along with its centred 3-year moving averages. While the deceleration in M4 ex-OFCs was extreme, so was the speed and extent of policy tightening. On a 3-year view, this does not yet qualify as the most significant monetary drought. Figure 3 provides another perspective, which is to consider the expansion of M4, with and without the OFC component, scaled by nominal GDP expressed at an annual rate. This reveals that, whereas the 2007-09 GFC was concentrated in the OFC sector, the disturbance to the inverse velocity ratio was of similar intensity, whether or not OFCs are included. The inclusive measure has already fully retraced its Covid-era diversion, but the exclusive measure has not, implying that weak M4 lending and M4 growth rates have yet to exert a meaningful constraint on UK inflation.

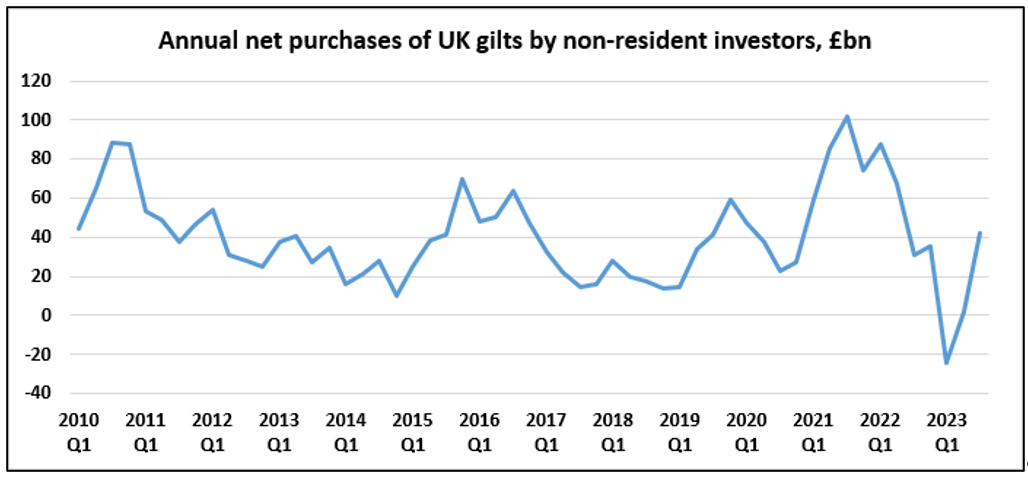

How can the UK retain an inflationary bias when the pace of broad monetary growth is so low? Firstly, because the household and private non-financial corporate sectors have excess money balances in relation to their expenditures. Secondly, because the public sector debt machine is running hot. The ratio of public sector net debt, excluding public sector banks and the Bank of England, to GDP at market prices rose from 85.1 per cent in the year to December 2022 to 88.7 per cent last year. This compares to a fall of 2.9 percentage points in 2021 and a rise of 0.3 percentage points in 2022. The leveraged LDI crisis has left an ongoing legacy with regard to the overseas appetite for gilts: the appetite has returned (figure 4) but must be enticed with much higher redemption yields.

Figure 1:

Data source: Bank of England

Figure 2:

Data source: Bank of England

Figure 3:

Data source: Bank of England and ONS

Figure 4:

Data source: ONS

*Adapted from a briefing by Baker McKenzie, “United Kingdom: The pensions LDI crisis – What happened next?”, 27 February 2023