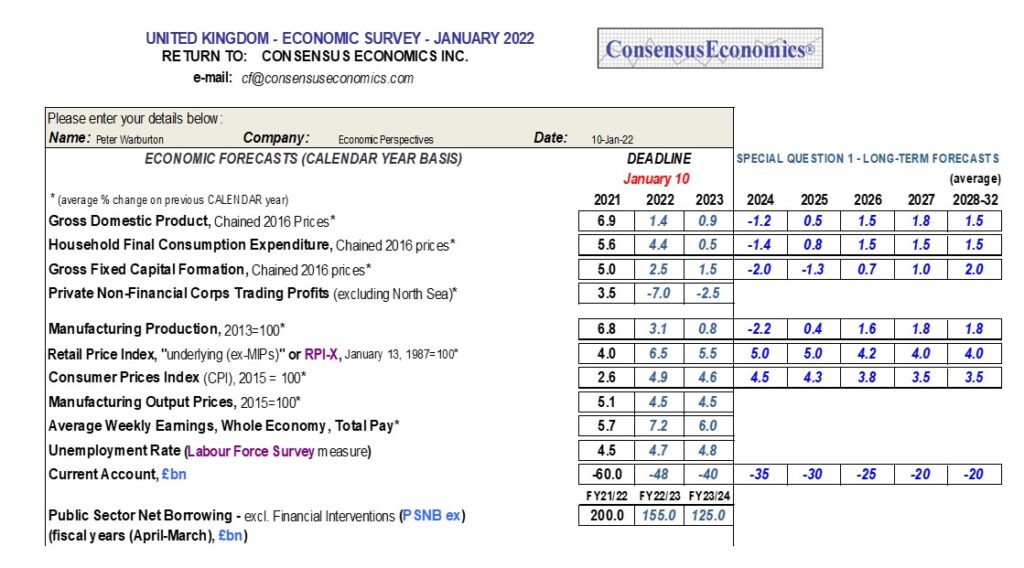

Following the publication in the Sunday Times of David Smith’s annual league table of forecasts of the UK economy for 2021, in which Economic Perspectives came first, we have decided to publicise our economic forecasts for 2022 and 2023. The numerical forecasts are shown in the table below. We begin with a brief commentary.

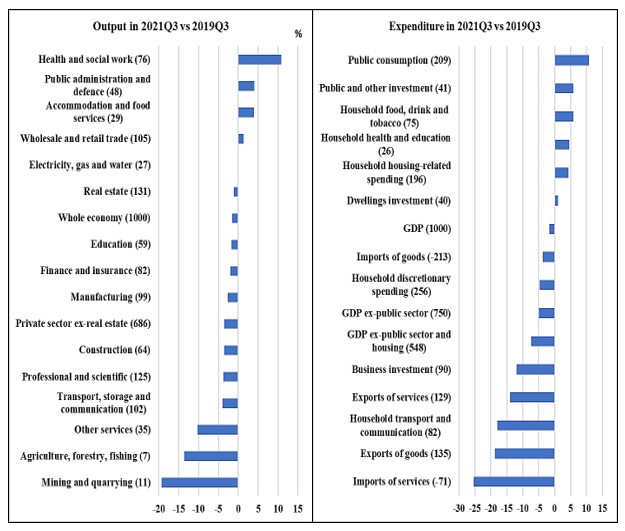

The full set of national accounts that appeared just before Christmas, covering the third quarter of 2021, afford an opportunity to examine the extent and nature of the recovery from the atrocious slump in the second quarter of 2020. There is an annoying tendency to assess progress solely in terms of the restitution of the pre-pandemic levels of output and expenditure. US, China, Korea and several other countries have already recorded higher readings for real GDP than before the pandemic struck, but the UK – in common with most European countries – has yet to do so. Yet, however much governments may wish us to believe that our economies have regained their prior composure and momentum, like a fallen rider re-mounting his horse, the detailed figures tell a very different story. The two charts below examine the changing structures of output and spending, comparing 2021Q3 with 2019Q3. There are numerous structural differences but the two most prominent are the expanded size and importance of the public sector and the housing market. The 1.6 per cent shortfall in overall GDP rises to 3.1 per cent after the exclusion of sectors in which the public sector is dominant, such as public administration, defence, education, health and social work, and to 3.5 per cent when real estate is also excluded. The expenditure analysis is even more revealing, suggesting that the removal of public sector elements reveals a 4.9 per cent private sector shortfall against 2019. If household expenditure on housing and fixed investment in dwellings is subtracted as well, the shortfall swells to 7.3 per cent. The economy that fell off the wall in March 2020 is structurally different from the patched-up version that is reaching back towards it. Business investment is 12 per cent lower, household discretionary spending on clothing, recreation, eating out, foreign tourism (net) and so on, is 4.7 per cent down from 2019. International trade volumes are painfully lower: over 16 per cent for exports and 10 per cent for imports. The UK private sector economy is still nowhere near the size that it was in late 2019. The understandable and necessary scaling back of public spending in 2022 will expose the distorted composition of recent economic growth and the implausibility of consensus growth forecasts.

In marked contrast to the consensus, we expect 2022 to be a challenging year for the UK economy, with real economic growth in the region of 1 per cent to 2 per cent rather than the professional consensus of 4 per cent. The detailed forecasts that we submitted on 10 January 2022 are shown in the table below.