2022 may not be the year of materially higher official short-term interest rates, but we can confidently predict that it will be the year of tighter credit. Credit tightening takes many forms in a complex financial system: withdrawal of subsidised lending, suspension of official purchases of credit instruments, raising of creditworthiness thresholds for borrowers, re-weighting of loan assets for capital adequacy purposes in the regulatory system as well as the nuanced increases in interest rates for different types of borrowers. A typical commentary infers that tighter credit means slower economic growth and lower inflation. This is not necessarily the case. Expect credit tightening to reinforce negative supply shocks in 2022.

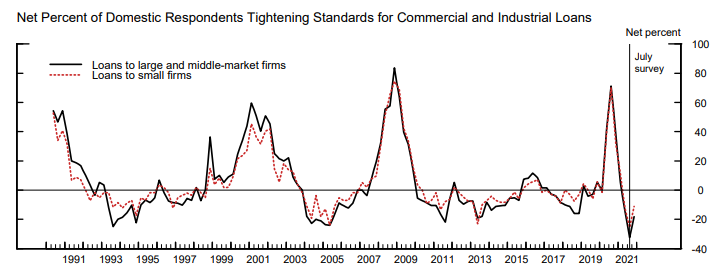

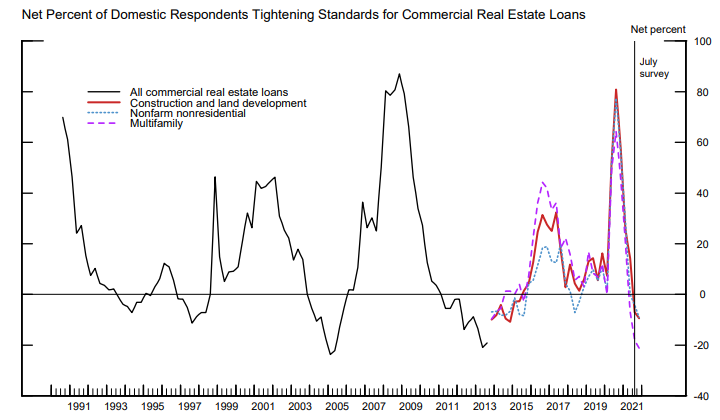

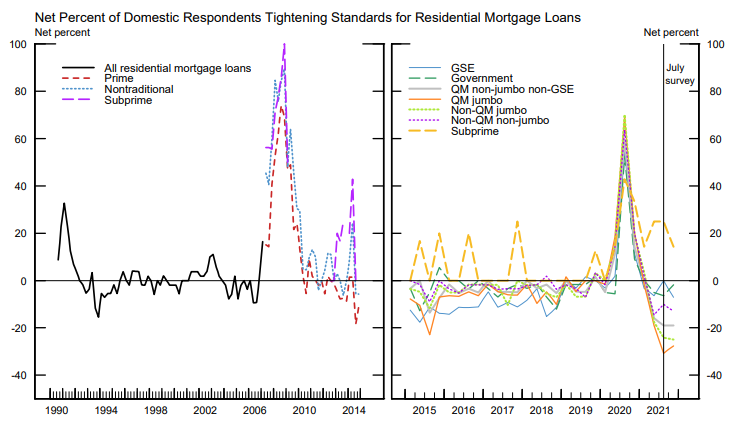

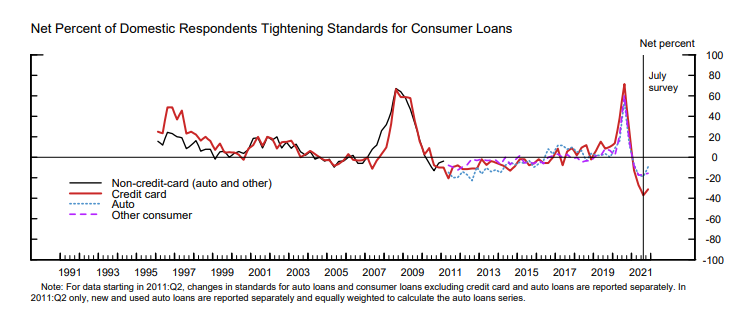

The October 2021 US Senior Loan Officers’ Lending Survey, published on 8 November, hinted at the approach of tighter bank lending conditions. Figures 1 to 4 reveal a definite upward tick for commercial and industrial loans and consumer loans, a whisper of change for residential mortgages and nothing at all for commercial real estate loans. A new survey is due in early February. The turning point in July 2021 is likely to be confirmed by the new survey, whilst still leaving the net percentage figures in negative territory.

However, like the proverbial swan, superficial serenity obscures a great deal of paddling below. Lenders are taking stock of their customers to determine which they would like to keep and which to shed. Bespoke pricing of credit using algorithms and various screening techniques allows lenders to raise the cost of credit for unwanted customers, incentivising them to take their business elsewhere. Likewise, the threshold of proof that new borrowers must reach to gain acceptance is likely to be raised. The truth is that lenders are fearful of taking on new business in a year when customers will be squeezed by inflation, taxes and deferred liabilities. Businesses that appeared to have survived pandemic-related losses may soon find that they cannot stand on their own 2 feet when supports are removed.

Credit tightening that restricts the cost or access to borrowing by consumers constitutes a demand shock and is commonly associated with weakening spending power, slower sales volume growth and weaker pricing. Credit tightening that restricts the cost or access to borrowing by marginal companies, on the other hand, limits the productive potential of the economy, weakens supply chains and reinforces the pricing power of large businesses. In the early 2000s, easy credit conditions granted access to marginal borrowers, facilitating the fracking boom and other types of mining and exploration activity. In the early 2020s, the boot will be on the other foot.

Figure 1

Figure 2

Figure 3

Figure 4

Data source: US Federal Reserve