President Biden was ill-advised when he allowed his latest, modest, legislative achievement to be named the “Inflation Reduction Act”. However noble the intentions of this ragbag of healthcare policies, tax legislation and climate investment, the one thing that it cannot claim to do is reduce inflation. In common with the emperor Diocletian, he has confused moral rectitude with monetary soundness. Before the president is tempted to institute a 1960s-style prices and incomes policy, enforced with or without the death penalty, he should know that their track record is diabolical.

The Inflation Reduction Act, which entails extra federal spending of US$433bn over 10 years, is the withered rump of the Build Back Better plan, originally tagged at US$3,500bn and latterly US$2,200bn. Passed by the wafer thin margin of 51-50, using the tie-breaking vote of VP Kamala Harris, the Congressional Budget Office reckons that the revenue-raising measures might just come out on top, to the tune of $10bn a year, on average. The Act’s claim to tame inflation by trimming medical and energy costs is delusional, regardless of its neutral funding implication.

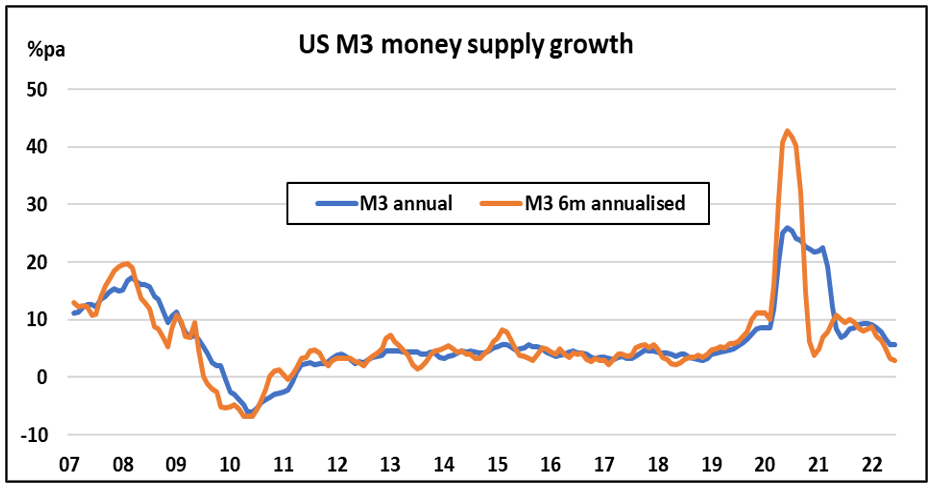

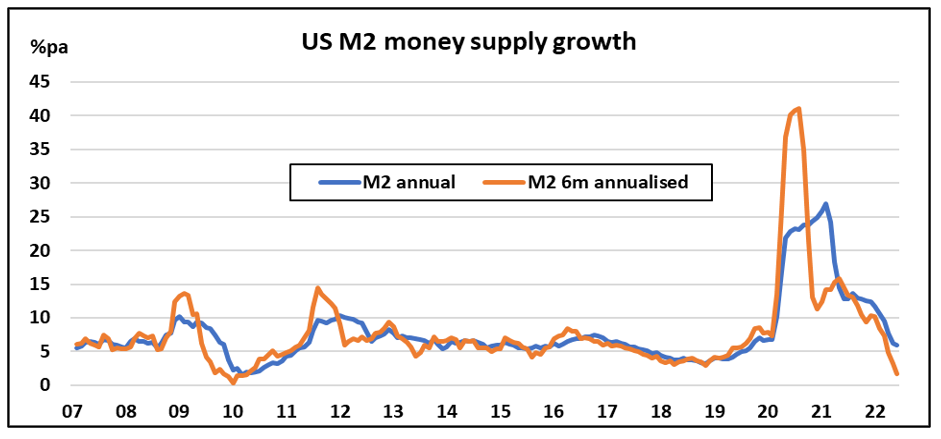

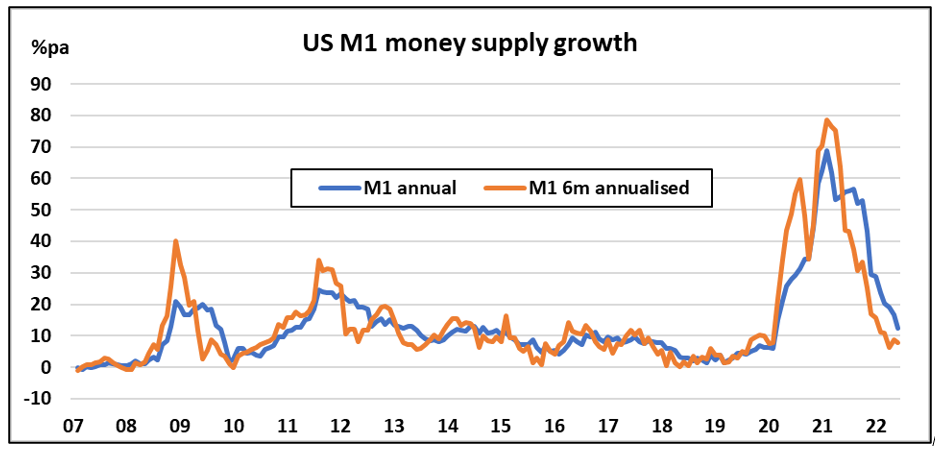

In recent years, we have rediscovered the recipe for inflation, allowing central banks such latitude in the expansion of their balance sheets (see figures 1,2 and 3) as to have macroeconomic effects on activity and prices. The serial debasement of the coinage in Roman times has been superseded by the debasement of fiat currencies by other means. The de facto monetary financing of Covid emergency spending measures has so inflated nominal purchasing power in the US and elsewhere, that shortages of materials, energy, consumer goods and services were inevitable. As the capacity to satisfy immediately the marginal addition to demand shrinks towards zero, the marginal price approaches infinity. The upscaling of prices is not (necessarily) about greed and profiteering, but rather a natural consequence of the overwhelming of short-term supply.

This is not to pour scorn on the sincerity of the ambition – to tame inflation – but as a reminder that sincerity, by itself, is no match for fiscal and monetary largesse. Witness this extract from a translation of the Diocletian Maximum Price Edict of AD301: “Whatever way everyone’s shared security demands our armies be directed, through villages or towns and on every route, effrontery goes to meet them with a spirit of thievery. It ratchets up the prices of things for sale, not fourfold or eightfold but so much that the human tongue’s reckoning cannot untangle what to call the accounting and the deed! In sum, meanwhile, by the purchase of one thing a soldier is deprived of his bonus and his salary: he yields to the detestable profits of robbers all the tax the whole world pays to support the armies. By their own hand our soldiers seem to give up the expectation of their own service and the labours they have completed to those who steal from everyone. In this way, day after day, the plunderers of the state itself carry off so much they don’t know they have it!

We have been moved by all these things that have been included above, rightly, as we should. Since human feeling itself seems to beg for relief, we have taken the position, not that we must set prices of goods and services for sale – nor indeed would it be thought right, since meanwhile very many provinces rejoice in the blessing of desired low prices as if by some special condition of abundance – but that we must set a limit. When some expensiveness should arise (the gods forbid it!) the greed that could not be restrained, as if it ranged in fields spread over some limitless expanse, will be choked off by the limits of our statute and the boundaries of a moderating law.

Therefore, we decree that these prices, which the written text of the subjoined abstract indicates, be kept by the observance of our whole realm: let all understand that license to exceed the same limits has been cut off in advance. As a result, in those places where a profusion of goods should noticeably abound, the benefit of low prices, which is very much the object of our care and foresight, is not hindered while greed, checked in advance, is restrained. Since, therefore, it is agreed that our ancestors too passed legislation for this reason, that effrontery should be repressed by the dread prescribed – because human nature left to its own will turn out altruistic only in absolutely exceptional instances, and dread, as a preceptor, proves to regulate duties most justly – we decree that if anyone should, in his boldness, strive against the form of this statute, he shall undergo a capital penalty. And let not anyone suppose that a hardship is being enacted, since the observance of restraint is present and available as a safe haven for avoiding the penalty.” As Murray Rothbard observed, “If anyone could force people to trade at the ceiling prices, Diocletian was the man. Yet the absolute emperor of the civilised world, a veteran general with myriads of secret police at his command, was soon forced to surrender. After a short interval, almost nothing was offered for sale, and there was a great scarcity of all goods. Diocletian was obliged to repeal the price-fixing Edict. Prices were finally stabilised in AD307 when the government stopped diluting the money supply.” The US monetary expansion has been tamed, but its consequences will linger.

Figure 1:

Source: Shadowstats (John Williams)

Figure 2:

Data source: US Federal Reserve, H6 release

Figure 3:

Data source: US Federal Reserve, H6 release

NB: M1 defined as currency plus demand deposits