The belated hawkishness of central banks is a wonder to behold. The currency of hikes, once depreciated to 15 basis points, quickly reverted to 25 basis points, then 50 basis points and 75 basis points. Talk of a full percentage point rise in the Fed funds rate is rife. Yet, like a chained dog that wakes from its slumber, its vigorous response is only good for the length of its chain. I concede that their chains are longer than I initially thought; but central banks are nevertheless constrained in their actions by the damage that their actions inflict on indebted economies and financial systems. Their political masters are not indifferent to credit failures, rising risk premiums and redundancies.

Central banks’ apparent freedom to “fight inflation” derives in part from general ignorance of the coming severity of the negative consequences for stressed personal, corporate and financial balance sheets. Around 2014, there was a marked shift in attitudes to debt in the English-speaking world. Bored with austerity and de-leveraging and lured by tempting low rates, borrowers began to push the boat out once more. Perched on vanishingly small capital bases, vast edifices of credit were constructed to transform low rates and thin spreads into decent annualised returns. Non-banks have been over-trading their capital, just as banks did before the GFC. Individuals have eroded their zero-yielding savings balances and have gambled their futures on the availability of perpetually cheap credit. The UK’s pension fund debacle over dodgy, leveraged investment strategies will not be an isolated example.

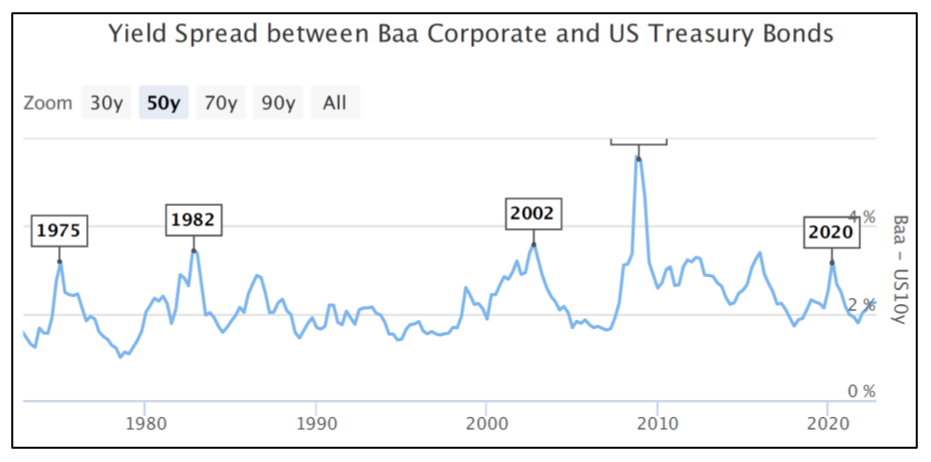

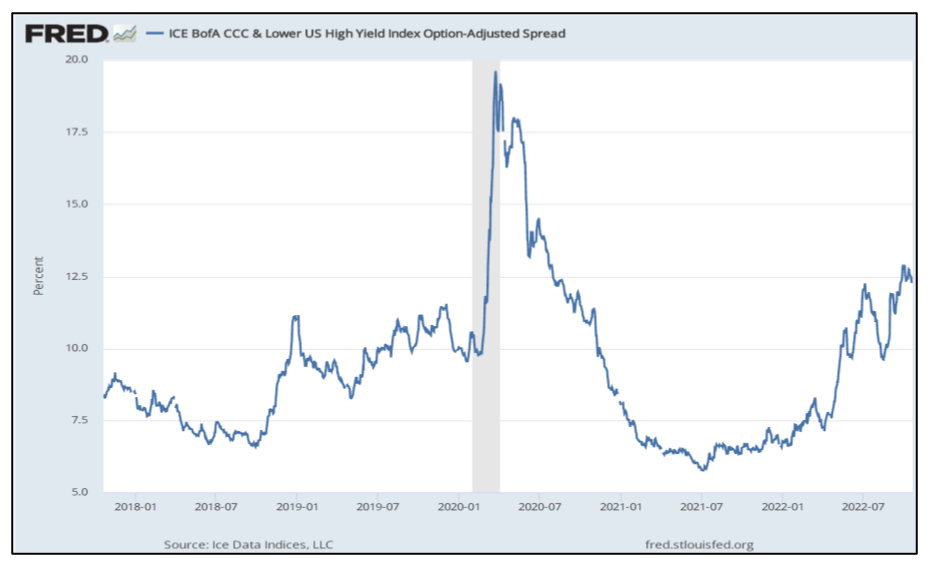

In an early-year blog (When credit conditions tighten, 27 January), I intimated that credit would tighten in 2022 irrespective of the extent of central bank interest rate rises (figure 1). After 13 years of obfuscation and financial repression, market borrowing rates are beginning to reflect market risks (figure 2). The widening of credit spreads – in corporate and sovereign debt – signifies the long-awaited return of idiosyncratic pricing in credit markets. It marks the end of the Bernanke-Greenspan era of “open all hours” sub-prime credit markets, which began in 2002. Some poor-quality issuers (figure 3) will no longer be able to roll over their debt; the door will be slammed in their faces. Distressed debt markets will come to life again as the supply of depreciated debt soars.

There is another mitigant of credit distress which has lengthened the central bank chain: banks have been falling over themselves to lend, even though the prospects of the borrowers are steadily deteriorating. This dynamic has weakened since the summer, but banks have offset some of the economic risk by failing to increase their deposit rates even as their lending rates track central bank actions. The risk-adjusted profitability of current lending is fading fast, but the banks may not recognise this for a while longer.

Once the politicians, and the banks, wake up to the delinquency and default scenarios that the central banks have triggered, then their chains will be yanked. Rather than a policy pivot, it will be a policy whiplash.

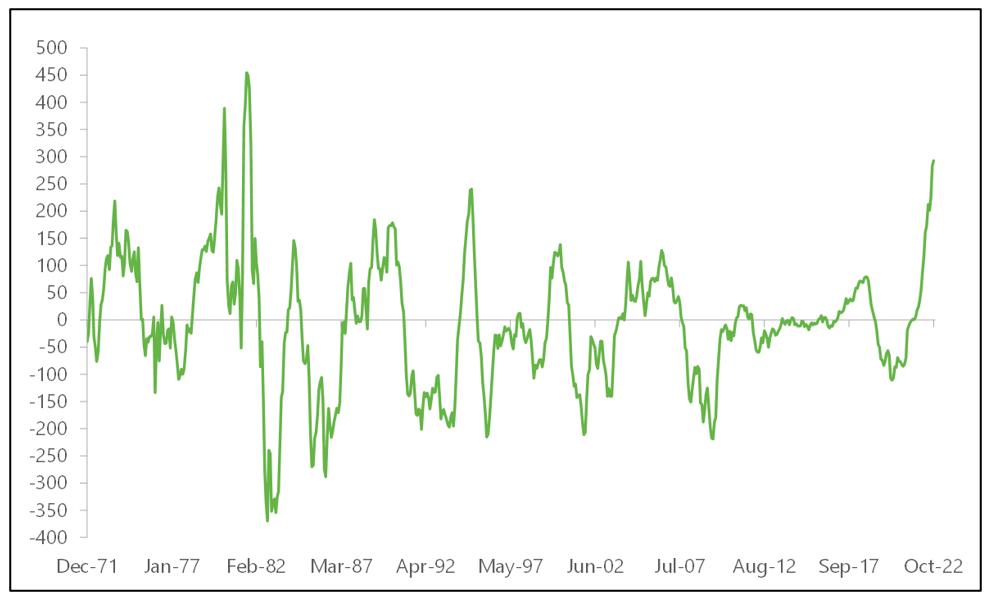

Figure 1: Annual change (in basis points) of GDP-weighted 2-year government bond yields

Source: Jamie Dannhauser, Ruffer LLP

Figure 2:

Source: Longtermtrends.net

Figure 3:

Source: FRED