Despite the marked acceleration of hourly wages over the past 12 months, the US labour market is as tight as a drum. The latest services ISM data confirms that there is sustained overheating of demand and elevated supply and labour shortages across service industries. Likely, the Federal Reserve will moderate its tightening programme in response to a lessening of price momentum over the next few months, leaving wage inflation to track higher still. Unable to “print workers” and unwilling to crush the economy, the Fed resembles a stranded goalkeeper who can only watch as the ball rolls across the line.

The Fed’s urgent tightening of monetary policy has depressed housing market activity but has so far failed to dent measures of labour market tightness. The demand for labour far outstrips the available supply, so readings are “off the scale”. The Biden administration is desperate for workers to return from their extended Covid sabbaticals, but the incentives for them to do so are weak. As Brian Pellegrini of Intertemporal Economics notes, “labour force participation has recovered most strongly among the youngest workers, both men and women, but results have been mixed in older age groups. Perhaps the most disturbing is the clear and consistent decline in participation among men aged 35-44″. Brian argues that the student loan payments holiday is a key factor in limiting participation, “generating a shortfall of low-skilled labour as college graduates with unmarketable skills leave the labour force”.

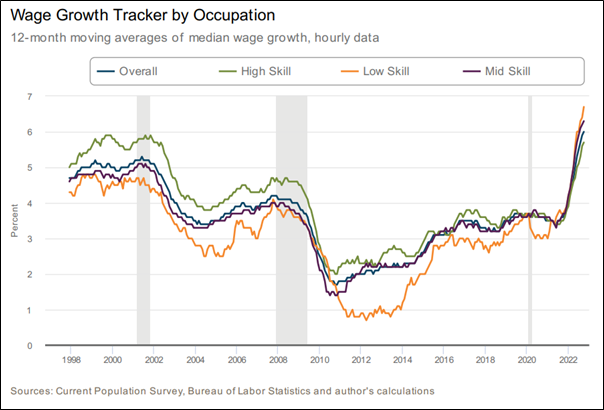

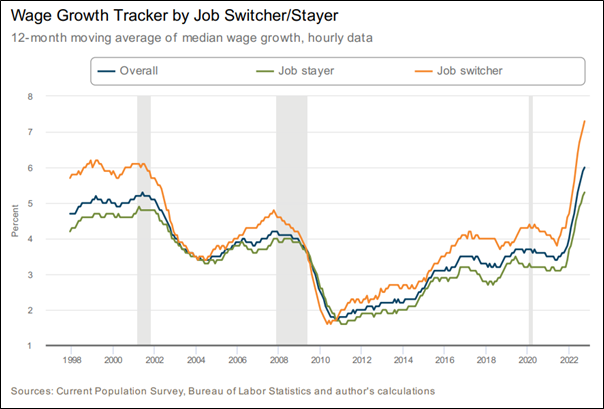

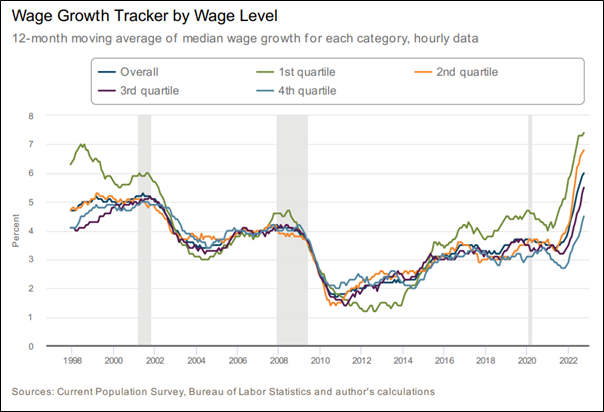

There is overwhelming evidence that employers still need to offer wage increases above the average to attract job switchers (figure 1). At 2 percentage points, the gap between the wage growth of switchers versus stayers is at its widest for 25 years. And the first (lowest) quartile of the wage distribution is enjoying the most rapid wage growth (figure 2), where the hit to labour participation is felt most keenly. Average hourly earnings of leisure and hospitality workers are up 6.4 per cent on a year ago. Conversely, the fourth (highest) quartile of the distribution shows the weakest increase in remuneration. Examples are the 2.8 per cent wage growth of miscellaneous services and 3.7 per cent for those engaged in financial activities. Finally, the wages of low-skilled occupations are rising faster than those of the high-skilled (figure 3).

There are three resolutions of this extraordinarily tight labour market. One, a Volcker-style monetary tightening that crushes demand, creates rampant financial discomfort and drives the inactive army of former workers back to the labour market for economic reasons. Two, a spontaneous improvement in productivity that enables demand for goods and services to be satisfied without an increase in staffing. Three, a progressive uplift in pay rates – and other forms of remuneration – that lures the recalcitrants back to work. If, as I suspect, the Powell Fed lacks the political freedom to pursue the first course of action and the second is a pipedream, then the most likely path is the third. The corollary of this extended wage acceleration is a squeeze on corporate earnings that the equity market seems unwilling, thus far, to acknowledge.

Figure 1:

Figure 2:

Figure 3: