Last week, US financial markets woke up to the depth of the funding and liquidity crisis that has been rippling around the fringes of the commercial banking system for a few weeks. Simply put, the members of the Federal Open Market Committee seem not to have understood the likely implications of shrinking their balance sheet after a year of steep interest rate increases. Commercial banks piggybacked the Fed in its large-scale acquisitions of Treasury and mortgage debt securities on the narrow regulatory pretext that these were zero or near-zero-weighted risk assets, without regard to their potential for capital destruction. While the Fed’s underwater securities portfolio is underwritten by the US taxpayer, the commercial banks’ underwater positions are not. Short-sellers and deposit withdrawals have brought down SVB, but the problem is systemic. The Fed has been removing chairs and there is no longer adequate seating capacity.

In an insightful academic paper published last October, former RBI governor Raghuram Rajan and his co-authors anticipated the dynamics that appear to be at work in the US banking system. They discovered that “during the initial period of the Fed balance sheet expansion, demand deposits issued and credit lines written by the commercial banks increase, while time deposits decrease. Importantly, the short-maturity, more demandable, claims written on liquidity do not fall significantly when QE ends or when the process of actively shrinking the Fed’s balance sheet during quantitative tightening (QT) starts. Instead, the ratio of demandable claims to reserves increases steeply over these periods. The authors refer to this phenomenon – whereby the banking system acquires more on- and off‑balance sheet demandable claims during QE that are not simply reversed during QT – as “liquidity dependence”, since it necessitates even greater central bank balance sheet support in the future”. (italics added)

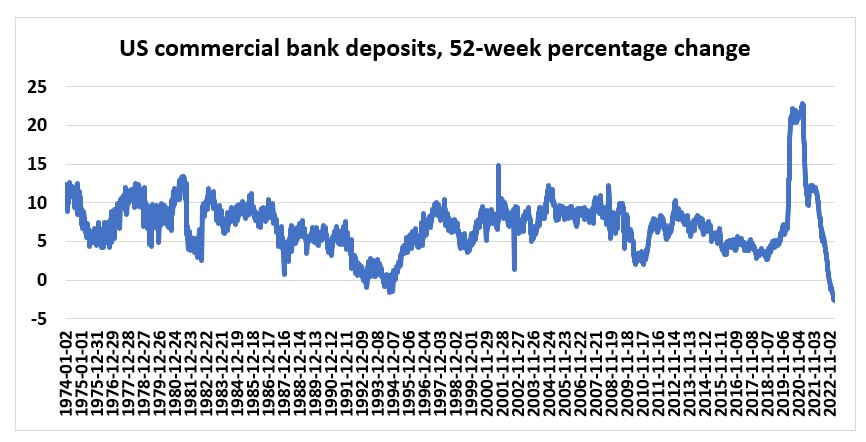

Figure 1 reveals that US commercial deposits are being withdrawn at the fastest annual pace in at least 50 years – probably since the Great Depression. Within an overall 2.9 per cent decline in total deposits since 13 April 2022, large time deposits have risen by US$376bn (26 per cent) while all other deposits have shrunk by US$896bn (5.4 per cent).

“Liquidity dependence may therefore explain why the financial system became more prone to liquidity accidents in 2019: the shrinkage of aggregate reserves without a commensurate decline in aggregate claims on liquidity was the likely deeper cause that left the system vulnerable and eventually dependent on further liquidity provision by the Fed.” Roll forward less than 4 years and the Fed faces the same dilemma: whether to pretend that the shrinkage of the balance sheet is a technicality as interesting as “watching paint dry”, in Janet Yellen’s memorable phrase, or to face up to the unfolding funding and liquidity crisis, cut rates and supply liquidity against collateral at face value.

If all this seems a world away from Jerome Powell’s semi-annual Humphrey-Hawkins testimony to Congress last Tuesday, it’s because it is. His rallying cry last week was “we will stay the course until the job is done”. His mantra was: “without price stability, the economy does not work for anyone”. How about, “without financial stability, the economy does not work for anyone”?

Figure 1:

Source: US Federal Reserve, H8 release, 10 March 2023