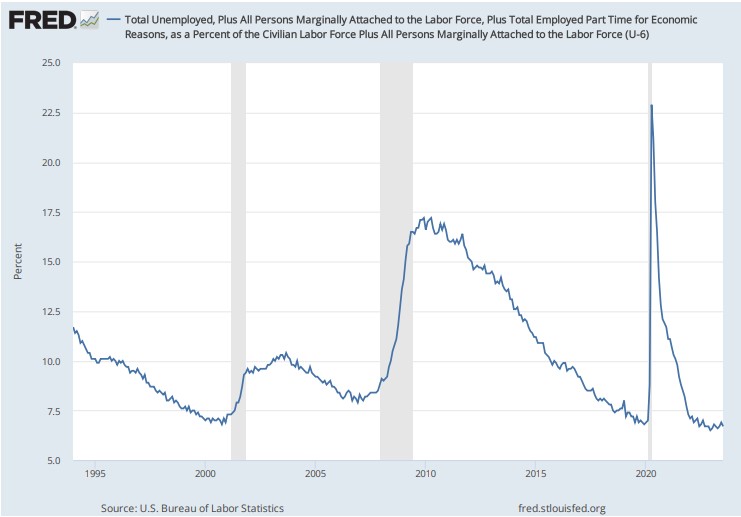

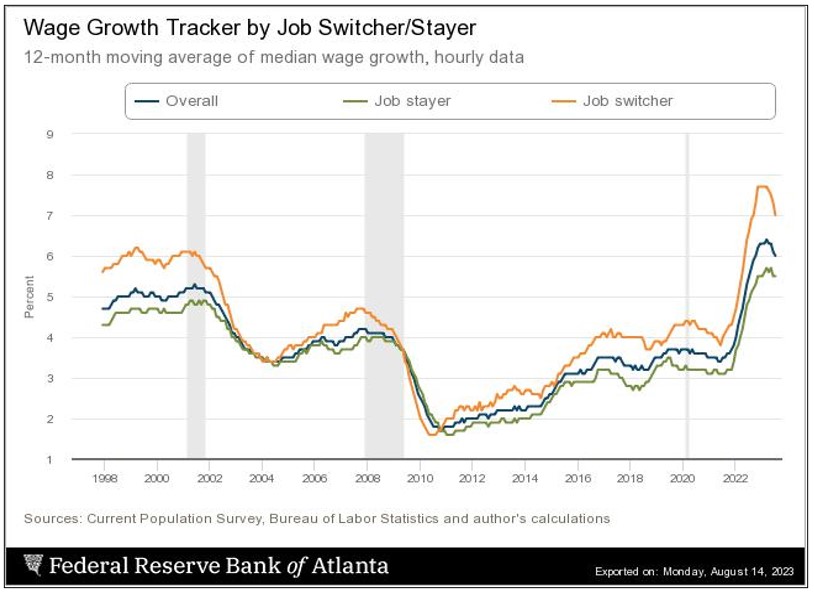

A softening of the pace of nominal US pay growth in recent months has been welcomed by policymakers as a sign that labour market tensions are easing, that the inflationary python is being wrestled to the ground. On closer inspection, employers are engaged in a pitch battle to attract and retain key staff. The gap between the wage growth of job switchers relative to job stayers remains wide and labour participation among the over-55s has failed to revive. The broadest measure of unemployment, the U-6, sits at 6.7 per cent, close to record lows. US wage growth will comfortably exceed the rate of CPI inflation over the coming year, supporting real household incomes and sustaining consumer demand at its exaggerated extent. Surveys of consumer inflation expectations confirm that workers are focused on a medium-term that contains much more inflation than the Fed’s 2 per cent per annum objective.

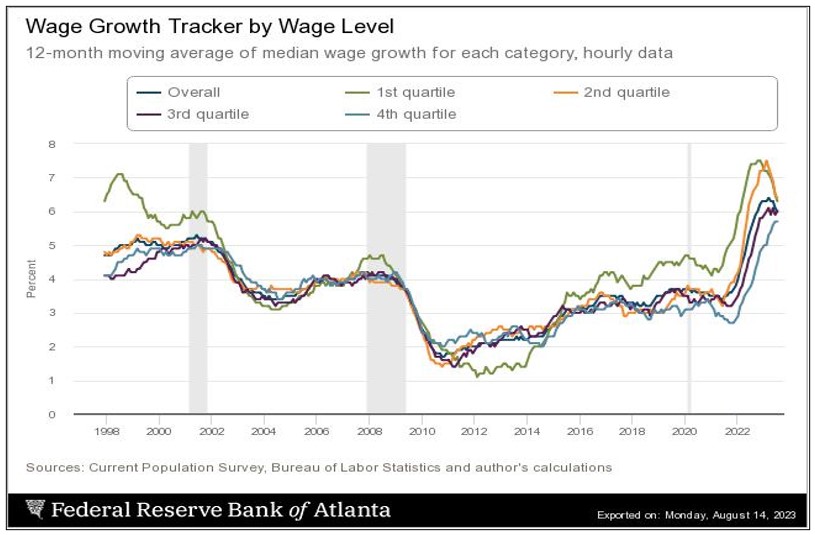

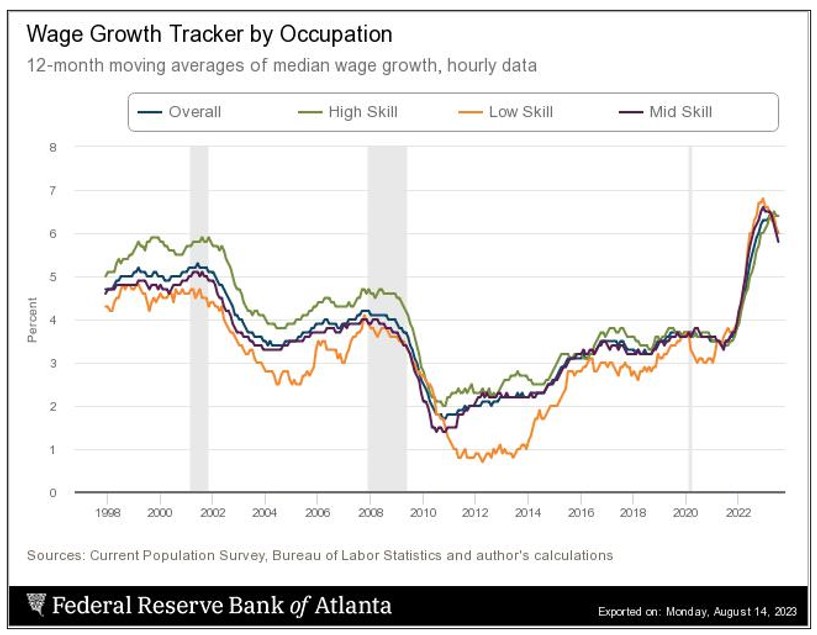

It is important to note that stubbornly high wage growth is not a product of collective bargaining; in fact, unionised labour forces have fared rather worse (3.6 per cent total compensation growth) than non-unionised ones (4.4 per cent) over the past year. Some of the apparent decline in annual pay growth is attributable to weaker bonuses and incentive payments. These are received disproportionately by the top quartile of employees by wage level. The employment cost index for civilian wages and salaries, excluding incentive-paid occupations was 4.8 per cent in the year to June 2023, barely lower than the 5.1 per cent of June 2022. This is also confirmed by the robustness of the increases achieved by lower-paid workers and those engaged in lower-skilled occupations.

The legacy of the pandemic is an epidemic of entitlement coupled with inactivity. To quote Brian Pellegrini, of Intertemporal Economics, “the misalignment between the vast supply of overeducated workers with few skills and an inflated sense of value and the huge demand for uneducated workers with real-world skills and a genuine work ethic will dog the US economy for years to come”. To make matters worse, the extravagance of the transfer payments made during the pandemic has created a buffer from reality for millions of older workers. That buffer is eroding steadily and by some measures has been almost exhausted. Can those who have granted themselves a state-sponsored ‘career break’ snap back into action and return to productive employment? After more than 2 years of idleness, the journey back to the work frontier is likely to be a tough one. Among those who are unemployed and looking for work, the percentage out of work for more than 15 weeks has risen from 31.5 in March to 36.9 in July.

The US is like a bus company, struggling to make ends meet. The buses are popular and full, but too many of the passengers are travelling on free passes. The bus company keep raising the fares, but this is scaring away the remaining fare-payers. And meanwhile the bus drivers keep leaving to take up better-paid driving jobs. The solution is to limit the entitlement to free passes and allow the demand for bus travel to fall. This will alleviate the wage pressure and help the labour market to stabilise.

Figure 1:

Figure 2:

Figure 3:

Figure 4:

To Pellegrini’s point: the year’s delay in bringing TSMC’s headline catching advanced Arizona fab on stream is down the lack of suitably skilled US staff to build it and then to operate it. The SIA and Oxford Economics reckon that the US based chip industry faces a near 70k skills shortage by 2030. Could be a serious brake on Washington’s ambition to source the advanced chips it will need onshore post 2025. As TSMC founder Morris Chang made plain to Nancy Pelosi when she visited Taiwan last year, a ‘hollowed out’, costly and overregulated US is actually a lousy place to set up an advanced chip plant.